Integration of hydrogen in electricity markets and sector regulation

Annual production of low-emission hydrogen could reach 38 Mt in 2030. At the beginning of 2020 China installed less than 10% of global electrolysers for dedicated hydrogen production. In 2022, installed capacity in China grew to 30%. By the end 2023 the capacity could reach 50%. Large amounts of government funding are being made available through schemes such as the US Hydrogen Production Tax Credit, the EU Important Projects of Common Projects European Interest and the UK Low Carbon Hydrogen Business Model.

Members

Convenor (TH)

Tongkum PIYATERAVONG

José LIMA (CL), Nattasak PAMORNPATHOKUL (TH), Christian ANDRESEN (NO), Dejan OSTOJIC (US), Zhaojun MENG (CN), Alfredo CARDENAS (CL), Gabriel VELASQUEZ (US), Achim WECHSUNG (US), ANSHUL GOYAL (CA), Caroline BONO (FR), Ben WU (AU), Nadim AHMAD / Santosh Kumar JAIN (IN), Jochen LINSSEN (DE)

Introduction

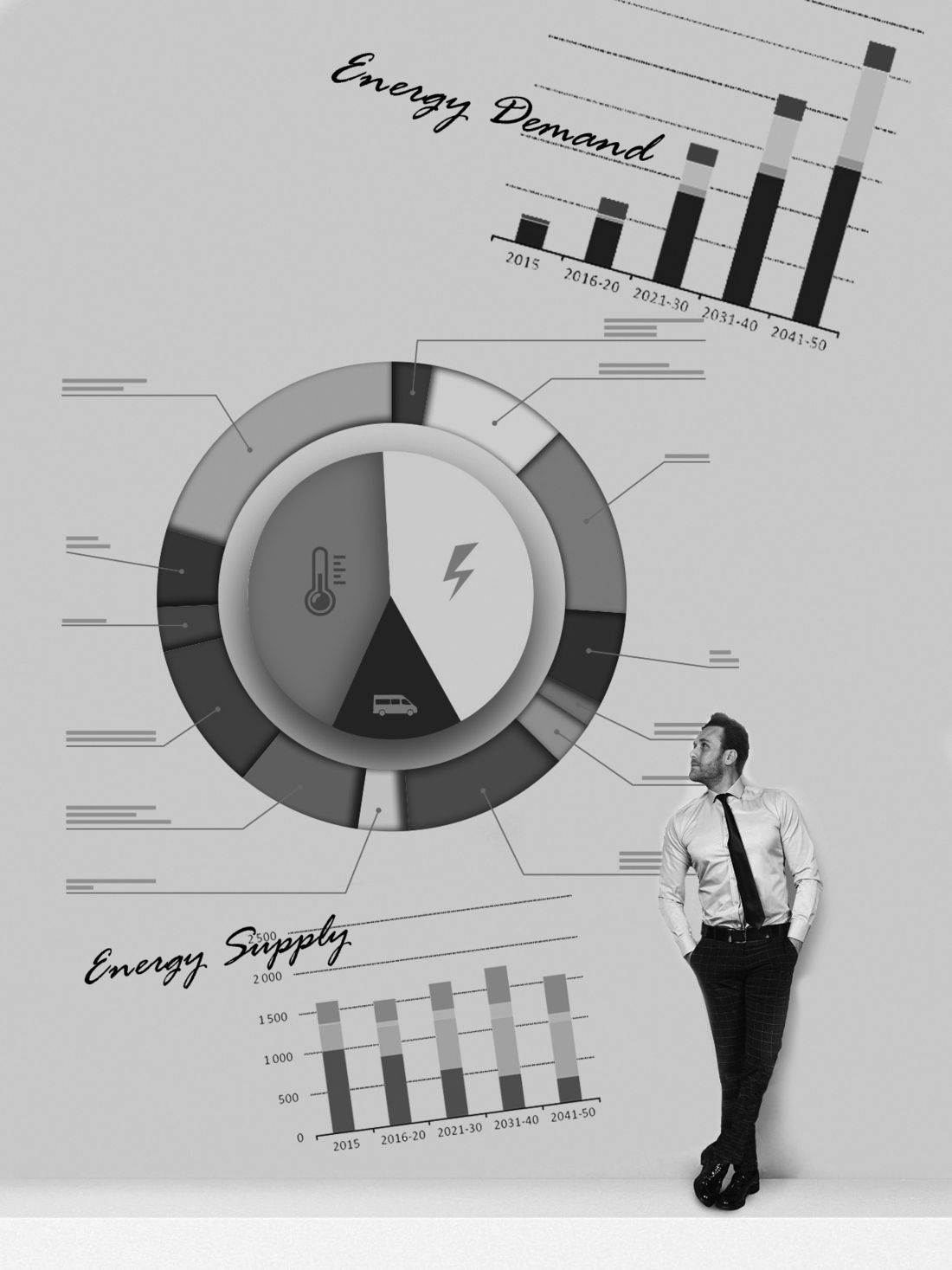

Government action has been focused on supporting low-emission hydrogen production, with less attention to the demand side. The private sector has started moving to adopt low-emission hydrogen through off-take agreements, but efforts remain at very small scale. International trade of hydrogen and hydrogen-based fuels is expected to be an important feature of scaling up low-emission hydrogen demand.

Several countries have started putting in place regulations on hydrogen’s environmental attributes and developing associate certification schemes. These have some commonalities, but also significant divergences, which may lead to market fragmentation. Referring to the emissions intensity of hydrogen production in regulation and certification—based on an agreed methodology—can enable mutual recognition.

Scope

Hydrogen can play an important role as energy absorption machine for abundant intermittent renewable energy such as wind and solar in low demand electricity consumption periods as well as energy transmission and distribution in certain areas where natural gas facilities are not available while wind and solar energy are readily available.

Hydrogen can be produced from various energy resources such as solar, wind, biomass, biogas, nuclear and others. This is similar to electricity, which it will challenge in resilient roles in energy supply.

Hydrogen can play a vital role as energy storage in seasonal peak shaving which can help minimize the need for dependable peak capacity in electricity production.

Hydrogen can be the non-fossil petrochemical feed stock in providing decarbonisation of the polymer industry.

Hydrogen can be developed to produce sustainable fuel in the transportation sector and increase countries’ readiness to be a net zero society.

CIGRE responded to the need to consider the role and certification of hydrogen in relation to electricity markets. The lead has been taken by Study Committee C1, Power System Development and Economics, with Working Group C1.48. Study Committee C5, Electricity Markets and Regulation then established two Joint Working Groups with SC C1. The first, JWG C5/C1.35, has produced this Technical Brochure (TB), which examines the integration of hydrogen into electricity markets. The second, JWG C5/C1.36, is examining the certification of hydrogen used to produce electricity.

Description of Technical Brochure

The structure of this TB is shown in Figure 1. The first chapter of the TB will focus on hydrogen production technology from various resources. This chapter will give an idea of the Levelised Cost of Hydrogen (LCOH) and Carbon Intensity (CI) for each type of hydrogen for better understanding and draw the demarcation line between low carbon hydrogen and green hydrogen even though they have the same chemical characteristics.

The next chapter will present hydrogen’s role as energy storage. Comparisons with other energy storage forms such as batteries in various energy storage functions and applications will be presented.

The TB will then describe how to transport hydrogen between regions/countries. Descriptions will be given of which technology is assumed most appropriate for given distances as well as energy loss and reasonable investment facility.

The key driver for a successful story with hydrogen is hydrogen consumption. Details will be given in this section. The importance of demand is in part due to the fact that demand commitment will bring sustainable investment projects. There are many technologies/services to be decarbonised, thus demand is highly changing. Stages of development are classified and explained in this section.

International hydrogen trading and markets are also important topics for CIGRE members, especially for SC C5 members who will be involved in power and energy markets which are being linked to carbon emission markets, renewable certificate and other Corporate Social Responsibility (CSR) certificate and greenhouse gas markets.

ELECTRA, is the digital magazine of CIGRE, you can obtain access as part of a CIGRE membership. Find out more about joining options here.

Other Technical Brochures