Carbon Pricing in Wholesale Electricity Markets

Due to increased concerns over climate change, many countries and jurisdictions around the world are implementing carbon-pricing schemes, mechanisms that apply a price to carbon and other greenhouse gas (GHG) emissions, to provide an incentive to reduce GHG emissions. According to the World Bank, as of 2022, there were 68 carbon-pricing initiatives implemented around the world. These initiatives span 46 national jurisdictions and 36 subnational jurisdictions and cover over 23% of global GHG emissions [1].

Members

Convenor

(US)

A. GIACOMONI

P.K. AGARWAL (IN), D. ALVARADO (CL), L. AMORIM (BR), A. BELOKRYS (RU), N. BOUCHEZ (US), K. BRUNINX (NL), Q. CHEN (CN), E. DELARU (BE), B. JOSEPH (AU), T. KASHIWAGI (JP), A. KAZAGIC (BA), G. LABUTIN (RU), R. MORENO (CL), S. MUKHERJEE (IN), R. ROLDAO (PT), A. RUDKEVICH (US), N. FURTAW (US), Y. THOMAS (FR), J. WRIGHT (ZA)

Introduction

There are two main archetypes of carbon pricing: emissions trading systems (ETSs) and carbon taxes. An ETS – sometimes referred to as a cap-and-trade system – caps the total level of GHG emissions. Tradeable emissions permits or allowances are issued, facilitating cost-effective abatement: each emitter makes the trade-off between abatement or paying for an emission allowance. By creating supply and demand for emission allowances an ETS establishes a market price for emissions. The cap ensures the required emissions reductions will take place to keep the emissions (in aggregate) within the pre-allocated emissions budget. Alternatively, a carbon tax directly sets a price on GHG emissions by defining a tax rate on GHG emissions or – more commonly – on the carbon content of fossil fuels. A tax differs from an ETS in that the emissions reduction outcome is not pre-defined but the price is. The challenge for the legislator is to set the tax to an appropriate level. In an ETS, in contrast, the carbon price is determined by the market but the emissions budget is left to the discretion of the legislator.

Regardless of the mechanism used to determine the carbon price, a carbon price can have a significant impact on wholesale electricity markets. Electricity and heat production are two of the largest sources of global GHG emissions. The burning of fossil fuels, including coal, oil and natural gas, for electricity and heat accounted for over 35% of global GHG emissions in 2021 [2]. While significant investments in zero-emission resources have occurred over the last decade, according to the International Energy Agency fossil fuels still accounted for over 61% of global electricity production in 2021 [3]. As a result, putting a price on carbon and other GHG emissions can considerably alter the system dispatch over the short-term and investment decisions over the long-term.

Scope/Methodology

While other studies such as those by the World Bank [4] provide an overview of existing and emerging carbon-pricing initiatives, Working Group (WG) C5.32 was established to examine their impacts on wholesale electricity markets and the electric power sector. This Technical Brochure (TB) examines the results of a survey on carbon pricing and wholesale electricity markets developed by WG C5.32. Several questions to be addressed in this TB include the following:

- What explicit carbon prices and companion policies currently impact wholesale electricity markets in each region?

- How have the carbon prices changed over time and what were the reasons for the changes?

- How have they benefit or hurt certain supply-side resources/technologies and have they created any reliability concerns?

- What are the impacts of carbon leakage and what approaches have been taken to mitigate leakage such as border adjustments?

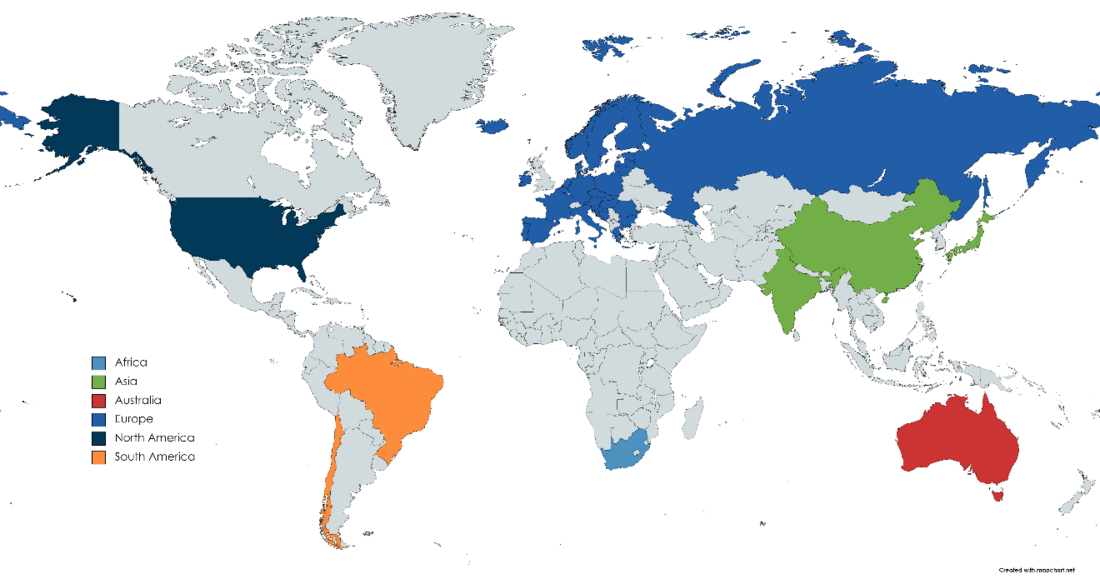

Countries and regions across all six continents were analysed including Australia, Bosnia and Herzegovina, Brazil, Chile, China, the European Union (EU), India, Japan, the Russian Federation, South Africa and the United States of America (US). Specifically, information was provided for 40 countries and 11 markets. The countries represented in the survey are shown in Figure 1. Note that individual responses were not provided for all countries in the EU.

Figure 1 - Countries that were represented in the survey

Description of the TB

The remainder of the TB is organized as follows:

Section 2: Carbon-Pricing Initiatives

For each of the 11 markets surveyed, a detailed description of the carbon-pricing initiatives that currently exist (or existed at some time in the past) that impact their wholesale electricity markets and the electric power sector are described in detail. A summary of the carbon-pricing initiatives for each of the 11 markets surveyed is shown in Table 1. Of the 11 markets surveyed, four include or included at one time an ETS, four include a carbon tax and three do not currently include any carbon-pricing mechanisms. For the Australian National Electricity Market (NEM), an ETS existed from 1 July 2012 to 1 July 2014 before it was repealed.

| Emissions Trading System | Carbon Tax | No Carbon Pricing |

|---|---|---|

Australia – NEM China - Guangdong Province European Union US - PJM Interconnection | Bosnia and Herzegovina Chile Japan South Africa | Brazil [1] India Russian Federation |

Section 3: Carbon Price Historical Trends

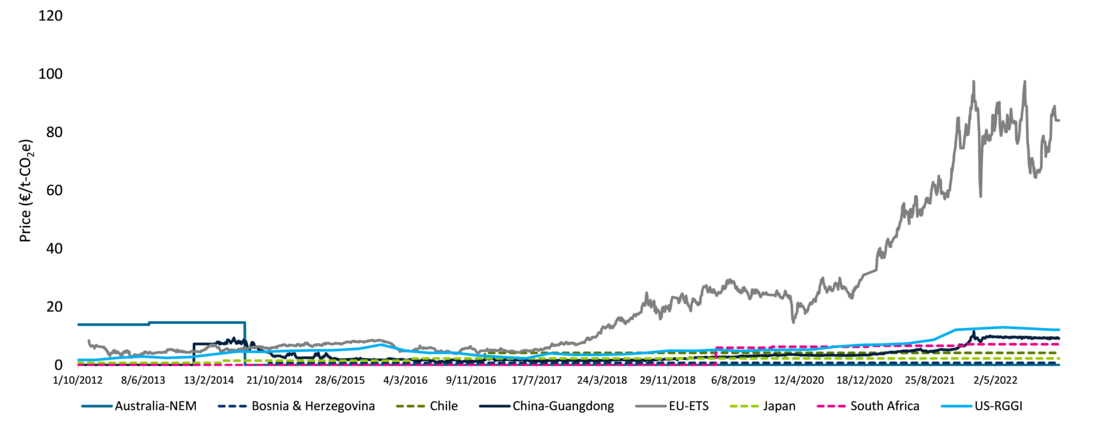

For each of the eight carbon-pricing initiatives described in Section 2, historical price trends are described. A comparison of the carbon prices for the eight carbon-pricing initiatives from October 2012 – December 2022 is shown in Figure 2. In Figure 2, all carbon prices have been converted to euros per ton CO2 equivalent using exchange rates in effect on 1 August 2020 to aid in the comparison. The carbon prices determined by an ETS are shown in solid lines and those determined by a carbon tax are shown in dashed lines.

As can be seen in Figure 2, with the exception of the Australia NEM’s carbon price prior to 1 July 2014, China Guangdong Province’s carbon price beginning in February 2022, the EU-ETS carbon price beginning in March 2018 and the US Regional Greenhouse Gas Initiative (RGGI) carbon price beginning in December 2021, all carbon prices remain under 10 €/t-CO2e. This observation underscores the political difficulty of implementing carbon prices that have significant impacts on the electric power sector and resulting GHG emissions, either directly by setting the carbon tax or indirectly by tightening the carbon budget.

Figure 2 - Comparison of carbon prices, October 2012 – December 2022 (ETS – solid line, carbon tax – dashed line)

Section 4: Companion Policies

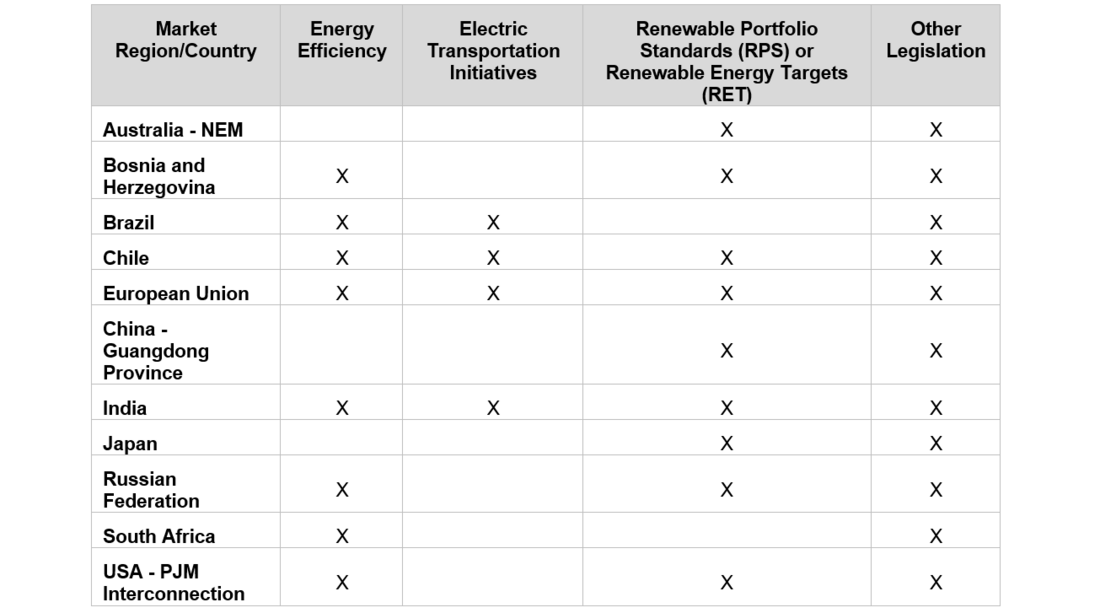

For each of the 11 markets surveyed, a description of companion policies aimed at reducing GHG emissions, in addition to any carbon-pricing initiatives, that impact their wholesale electricity markets and the electric power sector is provided. Of the 11 markets surveyed, eight currently have policies related to energy efficiency, four have electric transportation initiatives, nine have renewable portfolio standards (RPS) or renewable energy targets (RET) and all 11 have additional legislation related to reducing GHG emissions. A summary of the companion policies for each of the 11 markets surveyed is shown in Table 2.

Table 2 - Companion Policies for each of the Markets Surveyed

Section 5: Carbon-Pricing Initiative Impacts on the Power Sector

For each of the eight carbon-pricing initiatives described in Section 2, their impacts on their wholesale electricity markets and the electric power sector are analysed. One major trend that can be seen is that due to the low carbon prices in many of the carbon-pricing initiatives, as shown in Figure 3.1, their impacts on their wholesale electricity markets and the electric power sector is somewhat muted. However, as prices begin to rise, so will the magnitude of their impacts.

Section 6: Carbon Leakage Mitigation

Carbon leakage, as defined by both the EU and US-RGGI, is described below:

- European Union:

- The situation that may occur if, for reasons of costs related to climate policies, businesses were to transfer production to other countries or sectors with less stringent emission constraints, which could lead to an increase in emissions [5].

- The situation that may occur if, for reasons of costs related to climate policies, businesses were to transfer production to other countries or sectors with less stringent emission constraints, which could lead to an increase in emissions [5].

- US-RGGI:

- The concept that the RGGI CO2 compliance obligation and related CO2 compliance costs for electric generators could result in a shift of electricity generation from CO2-emitting sources subject to the RGGI CO2 Budget Trading Program to CO2-emitting sources not subject to RGGI [6].

Carbon leakage has the potential to diminish or in the worst case negate the emissions reduction benefits of any carbon-pricing initiative and is an area of ongoing debate in many regions. Approaches that have been implemented to mitigate carbon leakage for the carbon-pricing initiatives described in Section 2 are described in detail. Specifically, two of the initiatives (EU-ETS and US-RGGI) have implemented specific measures to mitigate carbon leakage while a third (Australia-NEM) had implemented specific measures before being repealed.

Section 7: Carbon Pricing Policies Under Consideration

Presently, several of the markets surveyed are considering either implementing a carbon-pricing mechanism or making changes to their current initiatives. Specifically, two markets (Bosnia and Herzegovina and China) are actively in the process of implementing an ETS for their region while four markets (Chile, the EU, South Africa and US-PJM) are actively discussing changes to their current carbon-pricing initiatives. Two markets have also recently announced plans to implement a carbon price (Brazil and India). Other markets are also engaged in discussions regarding carbon-pricing policies although definitive actions have not yet been taken. Carbon-pricing policies currently under consideration for each of the markets surveyed are described in detail.

Observations

One of the key observations that can be made is, with few exceptions, the persistent low level of carbon prices across each of the carbon-pricing initiatives studied over the last decade. These low carbon prices are driven by a combination of limited climate ambition (carbon budgets that are too high or carbon taxes that are too low) and overlapping climate policies (such as policies promoting renewable electricity generation), which, for example, drive down carbon prices in ETSs.

Despite the fact that carbon pricing is one of the most efficient ways to achieve emission reduction goals, implementing a carbon price that has a significant impact on the electric power sector and resulting GHG emissions is politically very difficult. As a result, with the recent exception of the EU, impacts on the wholesale electricity markets to date have been minimal. Nevertheless, as shown in Figure 3.1, nearly all the carbon prices are seeing an upward trend over the last couple years and as prices rise so will the magnitude of their impacts.

Alternatively, as described in Section 4, all the regions studied have been very successful in implementing companion policies aimed at reducing carbon emissions. Most companion policies put downward pressure on carbon prices. Despite the low carbon prices, there have been significant reductions in the carbon intensity of electricity production, which suggests that the reductions in carbon emissions in the electric power sector are being driven by companion policies.

Finally, few regions have implemented any measures to mitigate carbon leakage as discussed in Section 6. One of the reasons for this is the minimal impacts from the carbon-pricing initiatives on their wholesale electricity markets and the electric power sector due to the low carbon prices. However, if carbon prices continue to rise in the future, mitigating carbon leakage may become a much more important issue.

References

- The World Bank, "Carbon Pricing Dashboard," https://carbonpricingdashboard.worldbank.org/.

- M. Crippa, D. Guizzardi, M. Banja, E. Solazzo, M. Muntean, E. Schaaf, F. Pagani, F. Monforti-Ferrario, J.G.J. Olivier, R. Quadrelli, A. Risquez Martin, P. Taghavi-Moharamli, G. Grassi, S. Rossi, D. Oom, A. Branco, J. San-Miguel, and E. Vignati, "CO2 emissions of all world countries – JRC/IEA/PBL 2022 Report," Publications Office of the European Union, Luxembourg, 2022, https://edgar.jrc.ec.europa.eu/report_2022.

- IEA, "Shares of global electricity generation by source in the Net Zero Scenario, 2000-2030," https://www.iea.org/data-and-statistics/charts/shares-of-global-electricity-generation-by-source-in-the-net-zero-scenario-2000-2030.

- World Bank, "State and Trends of Carbon Pricing 2020," World Bank, Washington, DC, May 2020.

- European Commission, "Carbon leakage," https://ec.europa.eu/clima/policies/ets/allowances/leakage_en.

- RGGI, "CO2 Emissions from Electricity Generation and Imports in the Regional Greenhouse Gas Initiative: 2019 Monitoring Report," June 2022, https://www.rggi.org/sites/default/files/Uploads/Electricity-Monitoring-Reports/2019_Elec_Monitoring_Report.pdf.

- [1] Brazil has no carbon-pricing policy in place with impacts on the wholesale electricity market. There is a carbon-pricing policy in place, RenovaBio, but its scope is restricted to the reduction of emissions by fossil fuels from fuel distribution companies, mostly focused on the transportation sector. In May 2022, Federal Decree n.º 11.075/2022 set up the framework for establishing the Sectorial Plans for Climate Change Mitigation, which shall be jointly issued by the Ministry of Environment and the Ministry of Mines and Energy and establish progressive milestones for emissions reduction. Such plan has not yet been published for the energy sector.

Other Technical Brochures